The Benefits of Choosing to Purchase Reverse Mortgage for Your Home

The Benefits of Choosing to Purchase Reverse Mortgage for Your Home

Blog Article

Empower Your Retired Life: The Smart Means to Acquisition a Reverse Home Loan

As retirement approaches, lots of people seek efficient techniques to enhance their monetary independence and health. Among these techniques, a reverse mortgage arises as a viable option for homeowners aged 62 and older, permitting them to take advantage of their home equity without the necessity of monthly settlements. While this monetary device supplies several benefits, consisting of raised capital and the potential to cover crucial expenses, it is critical to comprehend the details of the application procedure and crucial factors to consider entailed. The following steps might expose how you can make a well-informed choice that might significantly influence your retired life years.

Comprehending Reverse Home Mortgages

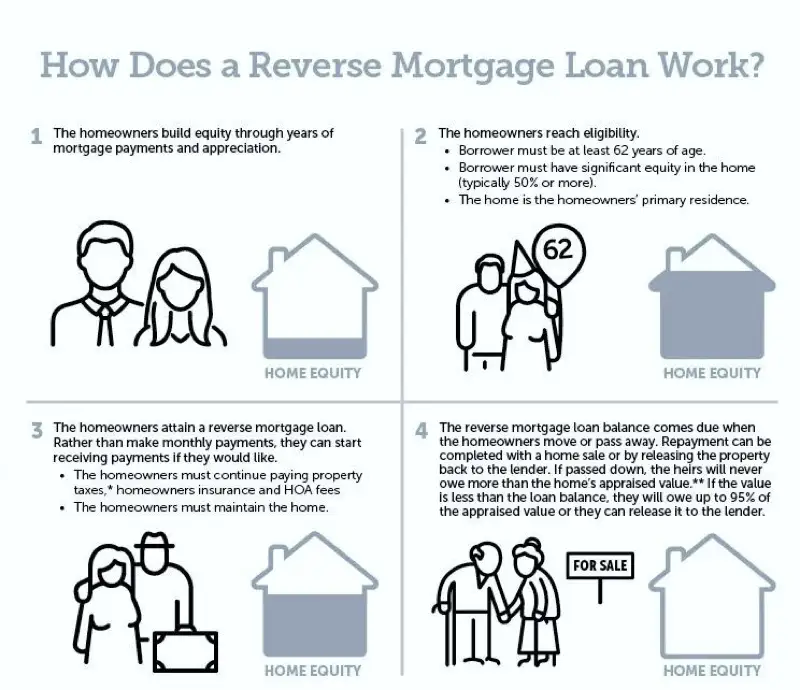

Comprehending reverse mortgages can be critical for property owners looking for economic versatility in retirement. A reverse mortgage is a monetary product that enables eligible house owners, generally aged 62 and older, to transform a portion of their home equity into cash. Unlike typical home loans, where customers make monthly payments to a loan provider, reverse home mortgages allow home owners to obtain repayments or a lump sum while maintaining possession of their home.

The amount readily available through a reverse home loan depends on numerous variables, including the home owner's age, the home's value, and existing rates of interest. Importantly, the finance does not need to be paid off until the property owner markets the home, moves out, or passes away.

It is necessary for potential customers to comprehend the ramifications of this monetary item, consisting of the effect on estate inheritance, tax obligation factors to consider, and ongoing obligations related to building maintenance, taxes, and insurance coverage. Furthermore, counseling sessions with certified specialists are often required to make sure that debtors fully comprehend the terms of the car loan. Generally, an extensive understanding of reverse home mortgages can equip property owners to make educated choices about their monetary future in retired life.

Benefits of a Reverse Home Loan

A reverse mortgage uses numerous compelling benefits for eligible home owners, specifically those in retired life. This financial tool permits elders to transform a section of their home equity into cash money, providing vital funds without the need for regular monthly home mortgage payments. The money acquired can be made use of for various functions, such as covering medical expenditures, making home renovations, or supplementing retired life income, hence enhancing overall economic versatility.

One significant advantage of a reverse mortgage is that it does not call for settlement until the homeowner vacates, markets the home, or dies - purchase reverse mortgage. This feature allows retirees to keep their way of living and fulfill unexpected expenses without the problem of month-to-month repayments. Additionally, the funds gotten are typically tax-free, allowing homeowners to utilize their cash without anxiety of tax obligation ramifications

In addition, a reverse mortgage can supply tranquility of mind, recognizing that it can act as an economic safeguard throughout challenging times. Homeowners likewise keep possession of their homes, ensuring they can continue residing in a familiar atmosphere. Inevitably, a reverse mortgage can be a calculated economic resource, encouraging senior citizens to manage their financial resources properly while appreciating their golden years.

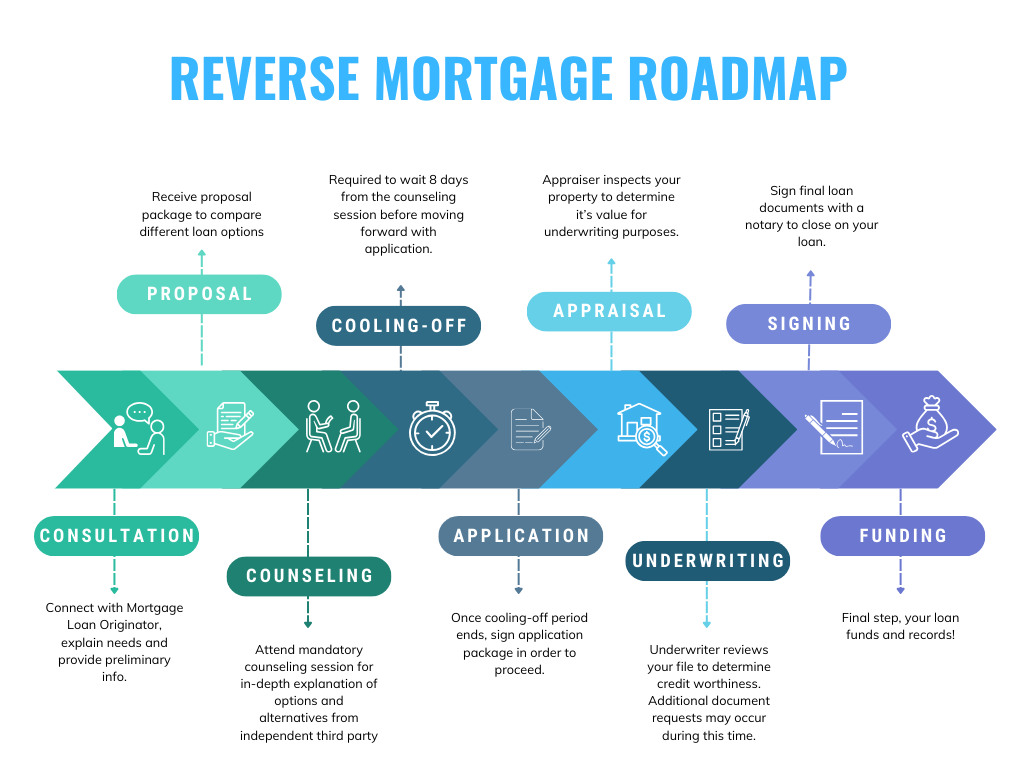

The Application Process

Browsing address the application procedure for a reverse home loan is an important step for property owners considering this economic option. The initial stage involves evaluating eligibility, which typically requires the property owner to be a minimum of 62 years of ages, very own the property outright or have a low mortgage balance, and inhabit the home as their primary home.

Once eligibility is confirmed, property owners need to undertake a counseling session with a HUD-approved therapist. This session guarantees that they totally comprehend the implications of a reverse home loan, consisting of the duties involved. purchase reverse mortgage. After finishing counseling, candidates can proceed to gather essential documents, consisting of proof of income, assets, and the home's worth

The next step involves submitting an application to a lending institution, who will certainly analyze the economic and property credentials. An evaluation of the home will likewise be carried out to establish its market value. If approved, the loan provider will provide funding terms, which should be examined thoroughly.

Upon acceptance, the closing more helpful hints process complies with, where last documents are authorized, and funds are paid out. Understanding each phase of this application procedure can dramatically boost the homeowner's self-confidence and decision-making concerning reverse home mortgages.

Trick Considerations Before Investing In

Investing in a reverse mortgage is a substantial monetary choice that needs careful consideration of a number of essential factors. Examining your economic requirements and goals is similarly crucial; figure out whether a reverse home mortgage straightens with your long-term strategies.

Furthermore, assess the effect on your present way of living. A reverse home mortgage can influence your eligibility for certain federal government advantages, such as Medicaid. Look for professional assistance. Consulting with an economic consultant or a housing therapist can give valuable understandings tailored to your specific situations. By thoroughly examining these considerations, you can make a much more educated choice regarding whether a reverse mortgage is the appropriate economic technique for your retired life.

Taking advantage of Your Funds

As soon as you have secured a reverse home loan, effectively handling the funds ends up being a top priority. The adaptability of a reverse home mortgage permits house owners to use the funds in various means, yet critical planning is crucial to optimize their benefits.

One crucial technique is to produce a spending plan that outlines your monetary goals and regular monthly costs. By determining required expenses such as healthcare, real estate tax, and home maintenance, you can allot funds as necessary to ensure lasting sustainability. Additionally, think about making use of a part of the funds for financial investments that can create earnings or appreciate in time, such as dividend-paying stocks or common funds.

Another important element is to preserve an emergency fund. Setting aside a get from your reverse home loan can aid cover unexpected expenses, supplying comfort and economic stability. Moreover, talk to a financial expert to check out possible tax implications and exactly how to integrate reverse home loan funds into your overall retired life approach.

Inevitably, prudent monitoring web of reverse home mortgage funds can enhance your monetary security, permitting you to enjoy your retirement years without the tension of financial uncertainty. Careful preparation and educated decision-making will make certain that your funds work successfully for you.

Final Thought

In final thought, a reverse home loan offers a feasible economic approach for elders seeking to improve their retired life experience. By converting home equity into available funds, individuals can resolve vital costs and secure extra financial sources without incurring month-to-month settlements.

Recognizing reverse mortgages can be crucial for property owners seeking economic versatility in retired life. A reverse home loan is a monetary item that permits qualified house owners, usually aged 62 and older, to transform a portion of their home equity into money. Unlike conventional mortgages, where debtors make monthly settlements to a loan provider, reverse home mortgages allow house owners to obtain payments or a swelling sum while keeping possession of their home.

Overall, an extensive understanding of reverse home loans can encourage home owners to make educated decisions concerning their financial future in retirement.

Seek advice from with a monetary advisor to explore possible tax implications and exactly how to incorporate reverse home mortgage funds into your overall retired life approach.

Report this page